Still Climbing

Quarterly review

Quarterly review

Richard Morin

Asmaa Saleem Malik

Another quarter, another sharp rise in stock markets. The 2 main components of the balanced portfolio - Canadian and U.S. equities - are up sharply again in Q3 2025: 12.5% and 10.4% (in $CDN) respectively.

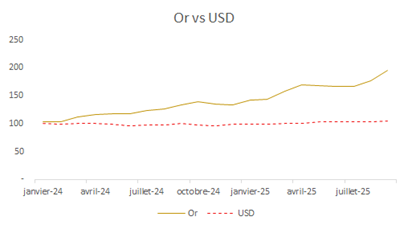

Although other sectors contributed to the rise, the performance of Canadian equities is largely explained by the seemingly inexorable rise in the price of gold. And there's no shortage of hypotheses to explain this craze for gold as a safe-haven asset, including an uncontrolled fiscal deficit and a mountain of debt in the United States, as well as the war in Ukraine and the threat posed to Europe by Putin's Russia.

It is these same risks that no doubt also explain why Bitcoin is close to its all-time high. Bitcoin as a safe haven? Not at Archer!

In the U.S., the 2 main factors behind the stock market's remarkable performance in Q3 were the (long-awaited!) Federal Reserve rate cut in September and what many observers consider to be a bubble in artificial intelligence-related stocks.

Combined with a reasonable year-to-date bond performance of 3%, this rise in equities explains the balanced portfolio's return of over 11% to date in 2025, and 15% per annum for the past 3 years. Even over 5 years, the annual return after fees is almost 9% for the balanced portfolio. Markets occasionally experience such periods of above-average returns. Sooner or later, a market correction will bring us back to the average - which is closer to 5-6% after fees for a balanced portfolio. But in the meantime, we're reaping the rewards.

As we explained in our last quarterly newsletter, these returns are also well above the assumptions used in retirement projections. For the majority of investors in the asset accumulation phase, whether in their thirties, forties or fifties, the best thing to do in the face of this windfall is probably nothing at all. You stay the course as long as you already have the right mix of stocks and bonds in your portfolio.

For many investors, however, this could be a good time to review certain aspects of their financial plan. Those approaching retirement, for example, who may have been planning to reduce the percentage of equities in their portfolio in order to reduce risk and increase current income, may decide to do so now.

Those who are already retired would also do well to review their financial projections. They'll probably find that they're "ahead" of projections made 2 or 3 years ago. If this is the case, they could reasonably aford spend a small part of that surplus to pay themselves a little bonus and take that trip they couldn't make during the pandemic, or make that purchase they've been dreaming of for a long time. You only live once!

Talk to your financial advisor.

Canadian equities continued their solid advance in Q3 2025, rising 12.5% and taking year-to-date gains to almost 24%. Materials led the way, jumping 37.4%, helped by a 17% rise in the price of gold. Energy and financials rose by 11.4% and 9.7% respectively, while information technology was up 13%, fueled by booming AI demand and solid corporate earnings.

US equities posted solid gains in Q3 2025, gaining 10.4% and taking year-to-date growth to 10.9%. Technology- and AI-focused companies led the way, with the IT sector emerging as the top performer.

NVIDIA, the chip giant, has consolidated its leading position in the AI sector, becoming the first US company to surpass a market capitalization of $4 trillion in July 2025. NVIDIA reached a market value of $1 trillion for the first time in June 2023 and tripled it in around a year, faster than Apple and Microsoft, the only other US companies with a market value of over $3 trillion.

Broadcom, the global technology leader in semiconductor and infrastructure software solutions, has reported robust third-quarter 2025 results, exceeding analyst expectations, driven by growth in AI-related technologies. The company reported third-quarter sales of $15.95 billion, up 22% year-on-year.

International equities gained 7.2% (in $CDN) in Q3 2025, taking year-to-date returns to 21.3%. Germany's €500 billion infrastructure plan marked a decisive step towards growth, signalling Europe's shift to a more expansionary fiscal policy.

Japan returned 10.4% in Q3 2025, buoyed by its trade agreement with the US, persistent yen weakness, an improving economy and attractive valuations. In addition, a rather technology-focused composition enabled the Japanese stock market to benefit from renewed enthusiasm for AI.

The MSCI Emerging Markets Index returned 12.1% (in $CDN) in the third quarter of 2025, up 21.9% year-to-date.

The US dollar index has fallen by around 10% since the start of the year in September 2025. This significant decline in the US dollar has helped to alleviate debt servicing pressures in emerging markets.

The Chinese stock market gained 23.4% in the third quarter, benefiting from a weaker dollar, which supported its export competitiveness and reduced the cost of servicing foreign currency-denominated debt. Market returns were also driven by optimism in technology and institutional flows. However, the market's exuberance was not sustained by economic strength, with growth remaining modest and consumer demand weak.

Taiwan's stock market continued its rally, rising 16.4%, supported by solid earnings in the technology sector (TSMC in center). Growing demand for AI/semi-conductors improved GDP/export forecasts and attractive valuations.

South Korea gained 13.1% as the third quarter of 2025 saw growing demand for AI-related chips, supported by key deals, such as Samsung's $16.5 billion contract with Tesla.

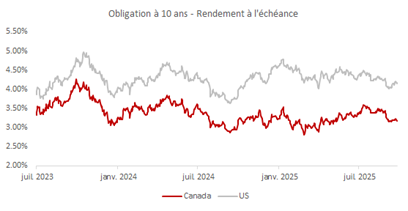

In the third quarter of 2025, 10-year Canadian government bond yields fell from 3.28% to 3.17%, as investors sought the safety of government bonds amid economic uncertainty, pushing bond prices higher. This demand for bonds was reinforced by the Bank of Canada's decision to cut its key interest rate from 2.75% to 2.5% in September 2025.

Canadian bonds generated a total return of 1.5% in Q3 2025, up 3.0% year-to-date.