Good Things Come in Threes!

Quarterly review

Quarterly review

Richard Morin

Asmaa Saleem Malik

A balanced portfolio, composed of 60% stocks and 40% bonds, generated a return of over 13% (before fees) in 2025. This marks the third consecutive year of gains exceeding 12%, more than double the return assumptions typically used in financial planning. Even over 5 years (8.4%) or 10 years (7.7%), the annual returns are significantly higher than expected. Excellent!

This performance reflects sustained S&P annual corporate profit growth (12.3% in 2025), as well as investors' high expectations for artificial intelligence. The stocks of the "magnificent 7" (Alphabet, Meta, Microsoft, NVIDIA, Amazon, Apple, and Tesla) account for a significant portion of this performance. They now represent more than 32% of the S&P 500's value, compared to 21% three years ago.

Canadian stocks have also performed even better. Their 31.7% return in 2025 is twice that of US stocks (12.2% in CAD). The inexorable rise in the price of gold (gold mining companies represent over 13% of the Canadian stock market index) largely explains this performance.

In such a context, where returns are concentrated in two sectors, active managers—who try to predict stock market movements or select stocks that will outperform the index—have had a very bad year. 94% of Canadian investment funds underperformed the S&P/TSX Composite Index by 2025. Their performance is hardly better over 10 years, as 97% have underperformed the index. By contrast, the balanced index portfolio managed by Archer has ranked in the top quartile of Canadian funds since the firm's launch in 2017 .

The reason stocks – particularly US stocks – have risen so much over the past three years is that investors bought them in anticipation of sustained profit growth, which they hope will result from the use of artificial intelligence. At nearly 28 times earnings over the last 12 months, the price-to-earnings (P/E) ratio is at its highest level since the tech bubble of the 1990s. Current stock prices are therefore already anticipating the good news to come.

In this context, 2026 should provide some initial answers to important questions regarding the future evolution of stock prices. Will the hundreds of billions invested in artificial intelligence by the likes of Alphabet, Amazon, and Oracle pay off? Will AI lead to increased productivity and profits for publicly traded companies? If not, a stock market correction is to be expected.

Canadian bonds returned 2.6% in 2025 and 4.4% annually over three years. This may seem low compared to stock market returns, but such a comparison is obviously unfair. Their time will come when investors collectively decide that stocks may have become a bit too expensive

Happy New Year to all!

The Canadian stock market was one of the best-performing developed markets in 2025, eclipsing its US counterpart, thanks to the gold sector which contributed over half of its 31.7% annual return.

The materials sector surged 98.2% in 2025 (+11.6% in Q4 2025) as economic uncertainty for much of the year drove investors toward gold as a safe-haven asset. This pushed gold prices to record highs and provided a strong tailwind for gold producers. Barrick Mining Corp contributed meaningfully, benefitting from higher gold prices and renewed investor interest following its announcement to explore an IPO of its North American gold assets. Basic materials stocks also gained support from rising prices for copper and other critical minerals, as investors sought protection against geopolitical and inflation risks.

The financials sector was the second-best performer, rising 30.8% in 2025 (+9.6% in Q4 2025). The Bank of Canada’s rate cuts during the year supported profitability by lowering funding costs and improving liquidity. Royal Bank of Canada helped drive sector performance, reporting strong Q4 net income of CAD 5.4 billion, up 29% from Q4 2024, on the back of higher net interest income and solid results across its main business segments.

U.S. equities rose 1.3% in Q4 2025, bringing YTD gains to 12.2%.

Healthcare (+11.2%) led the quarter, supported by strong demand for innovative treatments, higher pharmaceutical sales, and positive clinical trial news for biotech companies. Eli Lilly & Co stood out, driven by strong demand for its diabetes and obesity treatments and positive results from its new oral diabetes drug, boosting confidence in the company’s growth.

Communication Services (+7.0%) benefited from continued advertising revenue growth, streaming and content consumption, and strong demand for mobile and broadband services. Alphabet Inc. contributed to sector gains, driven by strong advertising revenue and rollout of AI-powered search and YouTube features that boosted engagement and monetization in Q4 2025.

International equities gained 3.1% (in CAD) in Q4 2025, bringing YTD returns to 25.0%.

Spain was the best-performing European market in 2025, delivering a return of 71.8% and 10.9% in Q4 2025, led by strong gains in banking, energy and renewable infrastructure stocks that helped the IBEX 35 outpace its European peers.

Japan posted a return of 1.2% in the fourth quarter of 2025, thanks to strong corporate earnings and continued structural reforms. In the United Kingdom, slowing inflation and strong economic activity enabled equities to post a solid return of 4.9%. These gains reinforced the importance of international investments for diversification and growth in balanced portfolios.

<span>The MSCI Emerging Markets Index returned 2.8% (in CAD) during the fourth quarter of 2025, up 25.2% YTD. Performance during the quarter was mixed across regions.</span>

China equities fell 9.1% during the quarter. The decline was driven by slower economic growth, ongoing government interventions in sectors such as technology and real estate, and trade tensions with key partners, which weighed on investor confidence and corporate earnings.

By contrast, Taiwan and South Korea posted strong gains, returning of 8.6% and 22.2%, respectively. Growth was driven by robust semiconductor and technology exports, with TSMC in Taiwan and Samsung and SK Hynix in South Korea benefitting from strong global demand, alongside resilient corporate earnings across key sectors.

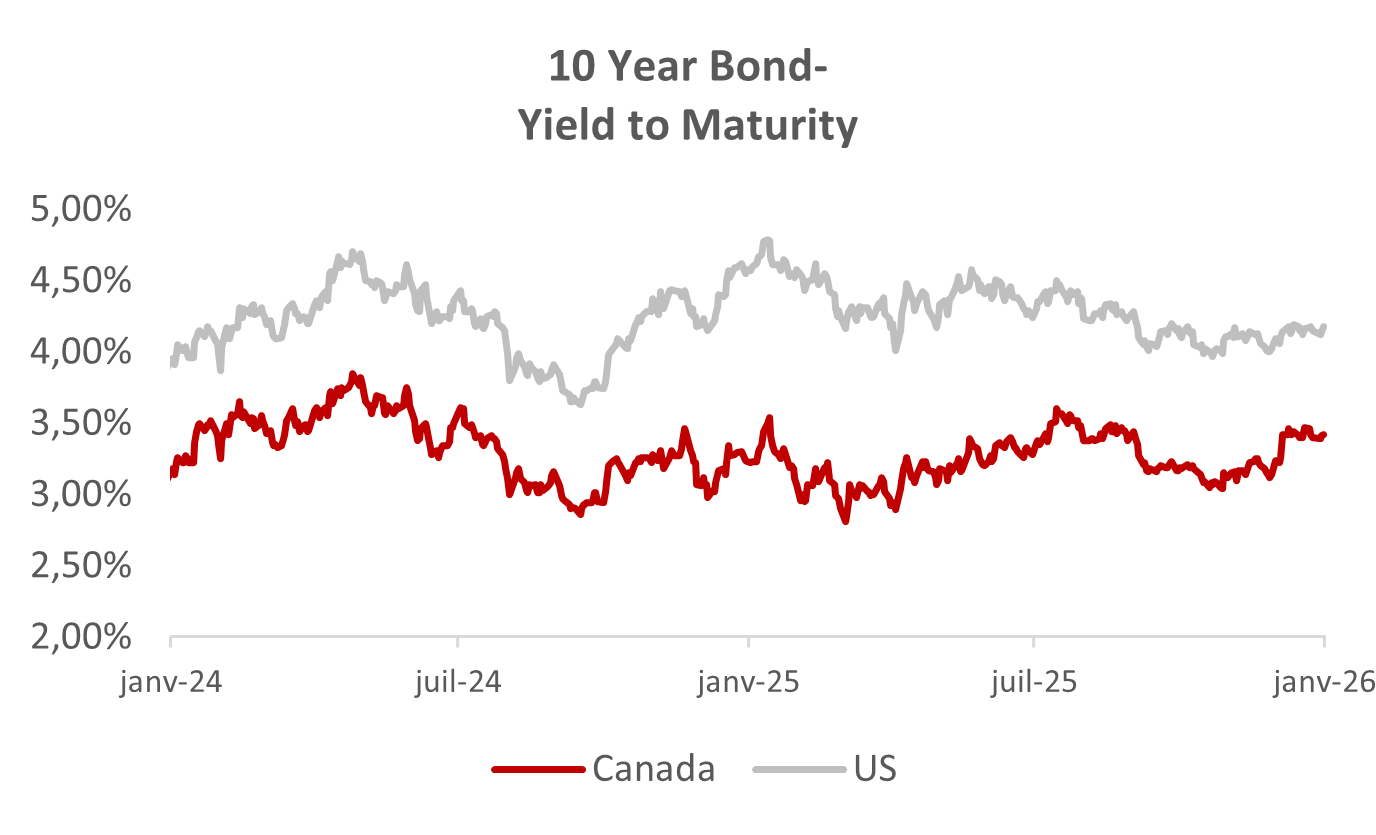

During Q4 2025, the 10-year Government of Canada bond yield rose from 3.17% to 3.41%, which led to a modest decline in bond prices over the quarter, as bond prices move inversely to yields.

The rise in yields was driven in part by changing expectations for interest rates. While the Bank of Canada reduced its policy rate earlier in the quarter to 2.25%, it held rates steady thereafter, signalling that the pace of further easing may be limited. This led investors to reassess the outlook for long-term interest rates and reduced demand for longer-dated bonds.

For balanced portfolios, fixed income continued to play an important stabilizing role. Importantly, the higher yield environment improves future income potential for bond holdings, supporting the defensive role of fixed income over the longer term.

Canadian bonds posted a -0.3% total return in Q4 2025, bringing YTD returns to 2.6%.

[1] FactSet, Earnings Analysis Report, December 19, 2025. The earnings growth figure represents consensus forward estimates.

[2] As of September 30, 2025, according to the Fundata database of Canadian mutual funds.