Resilience but...

Quarterly review

Quarterly review

Richard Morin

Asmaa Saleem Malik

Markets are showing remarkable resilience. Aside from a few bumps in the road in April, stocks and bonds have performed well since the start of the year, despite what could be described as serious headwinds.

Is the war in Ukraine - and Putin's alleged designs on other countries - threatening Europe's stability? No problem, European stocks are up 13.2% year-to-date.

Is Trump launching a global tariff war that threatens US corporate profits and raises the spectre of stagflation (economic stagnation coupled with persistent inflation)? Not to worry, the US stock market remains close to its record level, up 5.1% over the quarter and 0.4% year-to-date.

Could Canada be entering a recession, in part because of Trump's tariffs? Never mind, Canada's stock market is one of the best performers in the world (thanks to gold, as we'll see later).

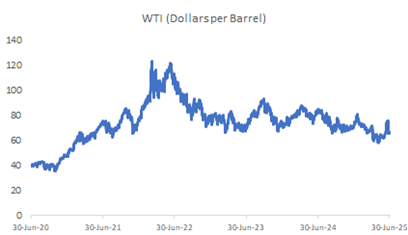

The Americans bomb an Iranian nuclear site, at the risk of further inflaming the Middle East. Oil prices are bound to soar, aren't they? Well, no. After a brief spike, a barrel of West Texas Intermediate costs less than it did at the start of the year, and about half its peak in 2022.

Congress is preparing to pass the Big Beautiful Bill, which will add trillions of dollars to the U.S. debt. Surely, bond buyers will balk! At least not for the moment. Yields on 10-year U.S. Treasury bonds are back where they were at the start of the quarter.

The return on the balanced portfolio (60% equities and 40% bonds) is 5.2% to date in 2025. Since the beginning of 2023, this portfolio has achieved an annualized return of 13.2%. Some will be tempted to treat themselves to a bit of luxury with these good returns, as indeed American consumers do. Still, it would be wiser not to spend all the "surplus", since you never know what's around the corner.

The very brief drop of over 10% in US equities triggered by the announcement of Donald Trump's Liberation Day tariffs (remember the penguins!) came as no surprise. What is highly unusual, however, is that bonds and the US dollar also suffered substantial declines during this volatile episode, whereas the opposite is usually the case: when the going gets rough, investors tend to take refuge in the "risk-free" assets that are US bonds.

Why did bonds and the dollar decline?

Because Trump's other big initiative, the Big Beautiful Bill, perpetuates the US fiscal deficit at its current level of 7% of the size of the economy. We learn in 1st year economics that such a deficit is unsustainable in the long term and will sooner or later lead to a fiscal crisis1. US Treasury bonds are therefore less perceived as a risk-free asset.

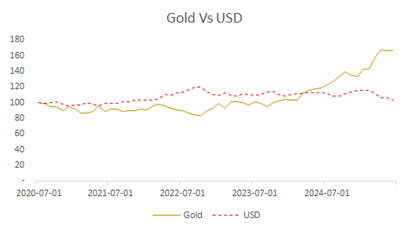

The tariff war and the Big Beautiful Bill also explain the 9% fall in the US dollar since the start of the year (the worst since 1973).

The other sign of stress is the seemingly inexorable rise in the price of gold, up 25% since the start of the year and over 40% in the last year. Since it is denominated in USD, the gold price is expected to rise when the dollar falls, in order to preserve its value, but its current rise also indicates that it is being partly substituted for US bonds in order to protect portfolio value.

Against this backdrop, Canadian investors who didn't put all their eggs in the US equity basket made good returns. Not only did the Canadian dollar appreciate against the US dollar, but Canadian equities benefited greatly from the rise in the price of gold - of which Canada is a major producer. If only American investors had taken our advice (Commentary - Q1 2024) and diversified their investments by buying Canadian stocks!

Have a great summer, everyone!

The Canadian stock market returned 8.5% in the second quarter of 2025, driven by strong performances from the financials (11.1%), information technology (14.2%) and materials (7.7%) sectors.

IT companies reported solid earnings, boosted by strong demand for AI. Major banks reported solid quarterly results, supported by stable credit conditions and sustained activity in their capital markets divisions. Rising commodity prices, notably gold, up 5% this quarter and 25% by 2025, supported the materials sector, helping to alleviate concerns about slowing economic growth. Investor confidence was also bolstered by the Bank of Canada's decision to maintain its key rate at 2.75%, as inflation showed signs of slowing.

US equities returned 5.1%, driven by technology and AI stocks. The quarter underlined the importance of remaining invested in a volatile environment, as well as the resilience of US equities, despite political and geopolitical uncertainty.

The best-performing sectors were information technology (23.5%), communication services (18.2%), manufacturing (12.6%) and consumer discretionary (11.3%). Struggling sectors were energy (-9.4%), healthcare (-7.6%) and real estate (-1.0%).

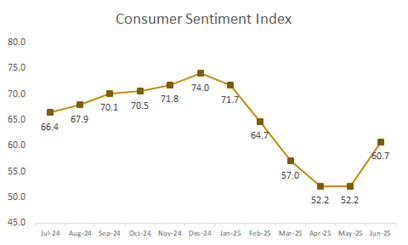

Consumer confidence dipped in April and May, weighed down by persistent fears of inflation, high interest rates and geopolitical uncertainties, notably US-China trade tensions and rising energy costs. However, there was an improvement in June, with the consumer confidence index reaching 60.7. This rebound is attributable to slowing inflation, stabilizing gasoline prices and a resilient labor market.

NVIDIA, the chip giant, has rebounded from a sluggish first quarter to launch a powerful new AI model, dubbed "Llama-3.1". Designed for smarter performance and greater efficiency, it demonstrates the company's continued leadership in AI development. NVIDIA shares jumped nearly 46% in the second quarter, confirming that AI hardware remains at the heart of investor optimism.

Broadcom, a global leader in semiconductor and infrastructure software solutions, has reported an excellent quarter, recording a 20% year-on-year increase in sales. These results underline Broadcom's central role in developing the technologies that are powering the AI revolution.

International equities continued their strong momentum of the first quarter, but experienced a more volatile second quarter. The period began with a wave of massive selling triggered by renewed global trade tensions, which briefly dented investor confidence. However, markets rebounded as trade concerns eased and inflation in the Eurozone continued to slow.

International equities returned 6.5% (in Canadian dollars) in Q2 2025. Within this universe, the MSCI Europe Index gained 6.4%, supported by moderate inflation, improving macroeconomic sentiment and fiscal stimulus in key markets such as Germany.

Japan returned 5.8%, rebounding from a decline at the start of the quarter thanks to renewed investor confidence, buoyed by a weaker yen, resilient domestic demand and strong export sectors.

The MSCI Emerging Markets Index returned 6.9% (in Canadian dollars) in the second quarter of 2025.

China's stock market fell by 2.6% in the second quarter, weighed down by escalating trade tensions between the US and China and persistent weakness in the real estate sector. Government stimulus measures provided some support, but failed to revive investor confidence.

The Indian market grew by 4.7% in Q2 2025, driven by strong domestic earnings, increased investor confidence amid easing geopolitical tensions and renewed political support.

Taiwan's stock market rose by 18.5%, buoyed by strong global demand for technology, particularly semiconductors, and easing fears of escalating trade tensions, with the US suspending some of its most aggressive tariff threats. Taiwan Semiconductor Manufacturing Company (TSMC) led the recovery of the Taiwanese stock market in the second quarter, thanks to its solid fundamentals and AI-driven demand momentum. South Korea posted a 27.4% performance, buoyed by improved foreign investor sentiment following the US decision to postpone the implementation of new reciprocal tariffs on its main trading partners until at least early July. This helped to stabilize the outlook for Korean exporters.

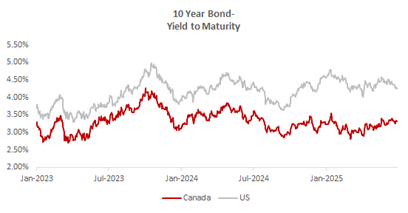

During the second quarter of 2025, the yield to maturity on Canadian 10-year government bonds rose from 2.97% to 3.28%, resulting in a slight decline in bond prices. This rise in yields was fuelled by a combination of domestic and international factors that boosted interest rates. High core inflation prompted the Bank of Canada to maintain its key rate at 2.75% in June, reinforcing the view that monetary easing remains unlikely in the short term.

Canadian bonds generated a total return of -0.6% for the quarter and 1.4% to date in 2025. While rising yields to maturity may lead to lower prices in the short term, Canadian bonds continue to play an essential role in providing income and stability within a well-diversified portfolio.

Note

[1] During a fiscal crisis, investors demand an exorbitant interest rate to buy government bonds, forcing the country to adopt drastic measures to reduce its deficit and debt. New Zealand in the 1980s and Canada in the 1990s suffered such crises.