A Stupid War

Quarterly review

Quarterly review

Richard Morin

Asmaa Saleem Malik

As of March 31, the balanced portfolio is down about 3.5% since the start of the war in Iran, wiping out all gains since the beginning of the year. At the time of writing, it is just under 1% below its all-time high. Nothing too alarming.

It's not surprising that the portfolio hasn't suffered too much from the war so far. Historically, wars haven't had a lasting impact on stock markets, which are much more interested in corporate profits—which continue to grow—than in the vagaries of geopolitics.

The real impact of war is unfortunately measured in human lives…

The other unexpected victim of the war appears to be the price of gold, which has fallen by about 110.9% since the start of the war on February 28, 2026. The problem with gold—unlike other assets—is that it doesn't generate any income. Its sharp rise since 2023 was primarily a speculative movement, and the war in Iran seems to have triggered a flight to sell. Moreover, some central banks also took advantage of the high price to sell off part of their gold reserves.

Another unexpected casualty of the war appears to be the price of gold, which has fallen by about 11% since the conflict began on February 28, 2026. The problem with gold—unlike other assets—is that it generates no income. Its sharp rise since 2023 was essentially a speculative move, and the war in Iran appears to have triggered a rush to sell. Not to mention that some central banks have also taken advantage of the high price to sell part of their gold reserves.

For everyone’s sake, let’s hope this stupid war will ends soon.

The Canadian stock market posted a return of 3.9% in the first quarter of 2026.

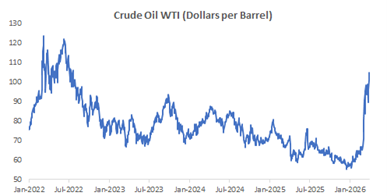

The energy sector was a standout performer in Q1 2026, boosted by rising oil and natural gas prices. Geopolitical tensions in the Middle East, particularly U.S.–Israel military actions against Iran, have raised concerns over potential disruptions to oil supply, driving prices higher. In March, West Texas Intermediate crude (WTI) exceeded $100 per barrel, marking an increase of approximately 56% relative to pre-conflict levels. Energy stocks helped support the TSX, offsetting weakness in other sectors.

The energy sector accounts for 17.9% of the S&P/TSX Composite Index, compared with just 3.8% of the S&P 500 Index. This overweight position has worked in Canada’s favor, enabling the Canadian market to outperform the U.S. market amid rising energy prices.

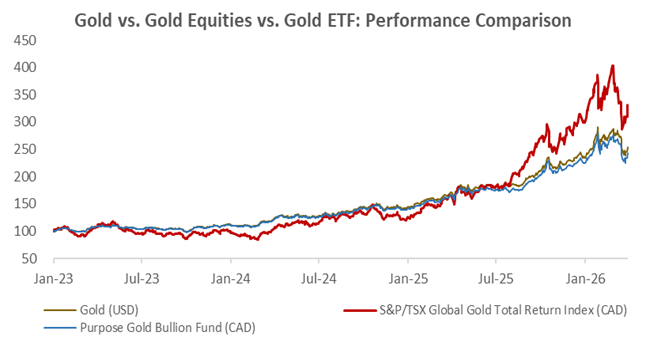

Gold was volatile in March 2026, falling from an early-month high of $5,311.6 to $4,392.3, a drawdown of 17.3%. The metal then recovered to $4,678.6 by month-end, resulting in an overall decline of 10.9% for March. While gold is usually considered a safe-haven, the early sell-off reflected short-term market pressures. Investors sold to raise cash or meet margin requirements, and rising interest rate expectations weighed on demand.

By the end of March, optimism that tensions with Iran could ease helped stabilize markets, allowing gold to recover some ground and reduce losses. Canadian investors benefited from the leveraged nature of gold equities, as the S&P/TSX Global Gold Total Return Index (CAD) — which tracks gold mining stocks — outperformed the metal itself over the quarter. Gold miners’ stock prices tend to amplify movements in gold prices due to operational leverage: when gold prices rise, profits increase at a faster rate than the price of gold. This effect translated into higher returns for investors holding gold-related equities.

The chart below illustrates this trend, showing the S&P/TSX Global Gold Total Return Index (CAD) in red, whose fluctuations are more pronounced than those of the spot gold price.

U.S. stocks fell 2.7% in the first quarter of 2026.

U.S. stock markets experienced high volatility in the first quarter of 2026, as the war waged by the United States and Israel against Iran heightened geopolitical risks, particularly around the Strait of Hormuz, a crucial energy transit route. Supply disruptions in the Middle East and the risk of a broader conflict strained the oil market, contributing to inflationary pressures and heightening investors’ concerns about costs.

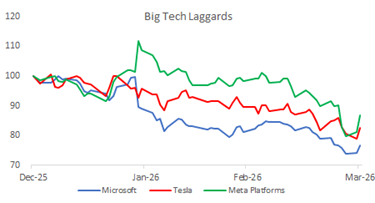

Market weakness intensified in March, with U.S. stocks falling 2.8% over the month. This broad-based decline affected all sectors, with the exception of energy, which benefited from the sharp rise in oil prices. The losses were primarily attributable to information technology, industrials, communication services, and healthcare, which accounted for the largest share of the market’s decline.

Weakness in technology and growth-oriented companies weighed on market performance. Microsoft fell 23.5% amid caution regarding cloud growth prospects following a previous sharp rise, while Tesla dropped 17.3% after first-quarter deliveries fell short of estimates. Meta also fell 13.3% as markets reassessed its valuation and growth prospects.

International stock markets rose 0.5% (in Canadian dollars) in the first quarter of 2026. Japan stood out with a 3.7% increase, driven in particular by Toyota, which reported strong global sales. Growth was driven by hybrid and plug-in hybrid vehicles, while the company increased its production of electrified vehicles to meet growing demand.

In contrast, the major European markets fell: France -3.6%, Germany -6.7%, Switzerland -2.4%, Spain -0.9%, Italy -2.0%, and Denmark -11.9%. The eurozone’s industrial sector got off to a poor start this year, with Eurostat reporting a 1.5% decline in production in January, well below the 0.6% growth forecast. Rising energy costs, persistent inflation concerns, and current geopolitical tensions—particularly the repercussions of the escalating conflict between the United States and the Middle East—have weighed on investor sentiment, dampening growth across the region.

Emerging markets rose 1.6% (in CAD) in the first quarter of 2026.

Taiwan rose 11.2%, driven by Taiwan Semiconductor Manufacturing Company (TSMC). Strong demand for AI-related chips and the company’s dominant position in cutting-edge semiconductor manufacturing supported robust revenue growth and attracted international investor inflows to this tech-heavy index.

South Korea surged 18.1%, led by Samsung Electronics following the announcement of the rollout of AI-powered 5G networks in partnership with Advanced Micro Devices (AMD) and the award of a 5G infrastructure contract with Canadian telecommunications operator Videotron.

Chinese stocks fell 7.0%, weighed down by weakness in the real estate market. Falling property prices have dampened consumer spending, slowed construction activity, and raised concerns about overall economic growth.

The Indian market fell by 16.7%, under pressure from growing geopolitical tensions in the Middle East and a sharp rise in crude oil prices, which led to significant outflows of foreign capital.

During the first quarter of 2026, the yield on 10-year Government of Canada bonds rose from 3.42% to 3.46%, causing their prices to decline slightly. However, coupon income offset this decline, enabling Canadian bonds to post a total return of 0.2% for the quarter.

This rise in yields reflects a readjustment of market expectations regarding future interest rates, inflation, and global risks. Additional upward pressure came from the yield on 10-year U.S. Treasury bonds, which rose from 4.18% to 4.30% amid geopolitical uncertainty, rising energy prices, and persistent inflation concerns.